Debt sucks people in like a black hole. The pull to spend more money is strong, the debt spirals, and it’s difficult to break free. Also, it’s hard on everyone — the person who owes the debt, and the person who services the debt.

Nobody likes getting a call from a debt collector, and nobody wants to be the person making that call, hassling and hustling fellow humans when they’re often at their lowest ebb. And if a debt collector contacts a customer who has become a debtor, they may have many concerns about whether the debt collection company is legitimate, whether the debt is theirs, or if the amount they are seeking to collect is accurate.

In recent years, the Consumer Financial Protection Bureau (CFPB) finalized two rules to collect debt from consumers: The Fair Debt Collection Practices Act (FDCPA) and its implementing regulation, Reg F CFPB, governing collection activities including prohibiting deceptive, unfair, and abusive collection practices.

With the recent update to the debt collection examination procedures incorporating the provisions of Reg F — the biggest change for the debt collection industry since the inception of the FDCPA will require Accounts Receivable Management (ARM) participants to re-examine their current CFPB Regulation F readiness programs to ensure they are able to comply.

The updates are primarily related to disclosure of the collector’s identity, the purpose/nature and time/place/frequency of communications and determining whether — the collector is engaging in false/deceptive/misleading communications or any harassing/abusive conduct.

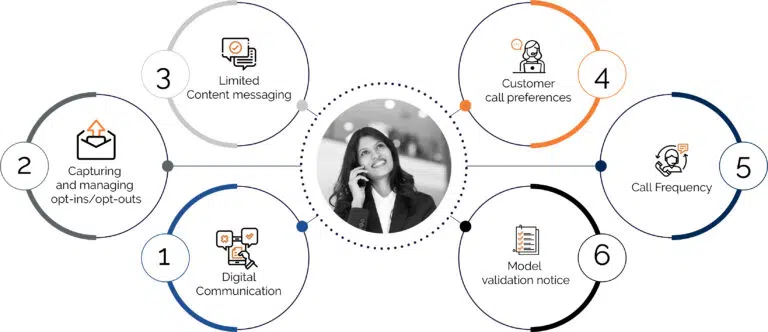

Here are six areas you need to address under Reg F to ensure customer-centric collections and be fully compliant to mitigate risks.

Six areas to address under Regulation F for Customer Centric Collections

Digital communication

Back in 2018, 73% of customers in late delinquency made a payment when contacted digitally — with email and SMS being the preferred methods of communication. Now, in 2022, digital is even more embedded, accepted and expected. Consumers demand digital, and lenders must embrace it to improve CX.

The rule provides for the use of digital communications — any misuse or unfair use of the digital channels by debt collectors such as spam labelling or publicly posting on a debtor’s Facebook wall, Twitter page, or Instagram comments instead of direct messaging can result in consequences for the collector.

Handpicked Related Content

Capturing and managing opt-ins/opt-outs

Reg F requires specific opt-in/opt-out processes prior to texting or emailing a customer. To start using omnichannel outreach, you need to first have opt-in consent based upon prior communications.

Electronic communication also needs to offer the consumer an easy way to opt-out of that channel for a specific email address/phone number. The debtor can use the medium to place a cease communication request or notify the debt collector that they refuse payment.

Limited content messaging

A definition for the term ‘limited-content message’ (LCM) is defined under the rule and implies that these are not considered ‘communications’. The definition identifies what information a collector may include when leaving voicemails for a consumer to ensure it is an attempt to communicate, NOT a communication about the debt itself.

When leaving a voice message — it qualifies as an LCM if the business name of the recovery agency does not indicate that it is in the debt collection business. Optional content to qualify can include salutations and suggested dates/times for replies to any of the debt collector’s representatives.

Customer call preferences

To succeed in a Reg F environment, it is also important to draw from the additional guidelines in the rule around ‘do not call’ requests, inconvenient customer time and place notifications, and individual preferences. This means collectors must mitigate errant call-blocking, digitally document preferences and leverage customer intelligence to gain insight into the best day/time and channel to reach the consumer.

A call aligned with insights into a particular customer’s behavior is likely to get a response. It is even more likely be answered if it is preceded by a text/email alerting the consumer of the imminent call.

Call frequency

The 7/7/7 rule on call frequency compliance — limits the frequency with which collectors can attempt to call debtors to seven calls over seven days, with no more than one call per day. If a collector speaks with a debtor over the phone, they must wait seven days before reaching out again, unless the debtor has given permission.

There are some exceptions to the rule including busy/out of service numbers, calls placed with prior consent and to authorized third parties. It’s important to note that the rule focuses on each debt/person which means that if a phone number is listed under several different debts, each can be treated as separate contacts.

Regulation F model validation notice

Reg F includes a debt validation notice template, also known as model validation notice (MVN), with new content/formatting guidelines. The rule provides certain legal protections to debt collectors who use the MVN to deliver validation information to consumers.

Hence, it is extremely important to check and re-check that the data you put in your model validation notice is accurate and letters which do not contain the required information are at risk of violating the law and operating outside of a safe harbor or be subjected to an expensive lawsuit.

So how do you stay compliant with the CFPB’s new requirements?

The CFPB Regulation F ruling on digital communications for debt collections has paved the way for a new dimension to the Receivables Management industry by modernizing debt collection laws and making it simpler for both debt collectors and consumers to understand their rights.

A robust compliance management system is critical for debt collection. Also having crucial conversations with your customers regarding the rules is essential for a smooth transition.

Empowering associates with Intelligent Automation tools to boost insights and ensure customer interactions do not run erringly of Reg F will enable you to deliver personalized and fully compliant services.

If you have any questions on the right technologies to help you remain compliant with Reg F, you can contact us here for a consultation.

If you need help steering the complexities of the new rules, please consult our compliance team for more information.

Featured resource

Download our whitepaper Collections of the future – A study by Everest Group to learn about the key considerations for lenders as they design a future-ready collections model.

Note: This blog is not intended to be legal advice or a complete explanation of the law in any area and should never be used to replace the advice of a legal counsel.